Inflation: The Invisible Tax on your Savings

Since the U.S. economy emerged from the COVID-19 pandemic, inflation has been a constant topic of discussion. According to data from US Inflation Calculator, in the years following the pandemic, the economy experienced a sharp surge in inflation, peaking at 9.1% in 2022 with an average of approximately 4.4% yearly between the beginning of 2021 and end of 2025. At its core, inflation reflects a sustained rise in the overall price of goods and services across the economy, which results in the gradual loss of purchasing power for people across the economy. American Economist Thomas Sowell frames it like this, “Inflation is in effect a hidden tax. The money that people have saved is robbed of its purchasing power.”

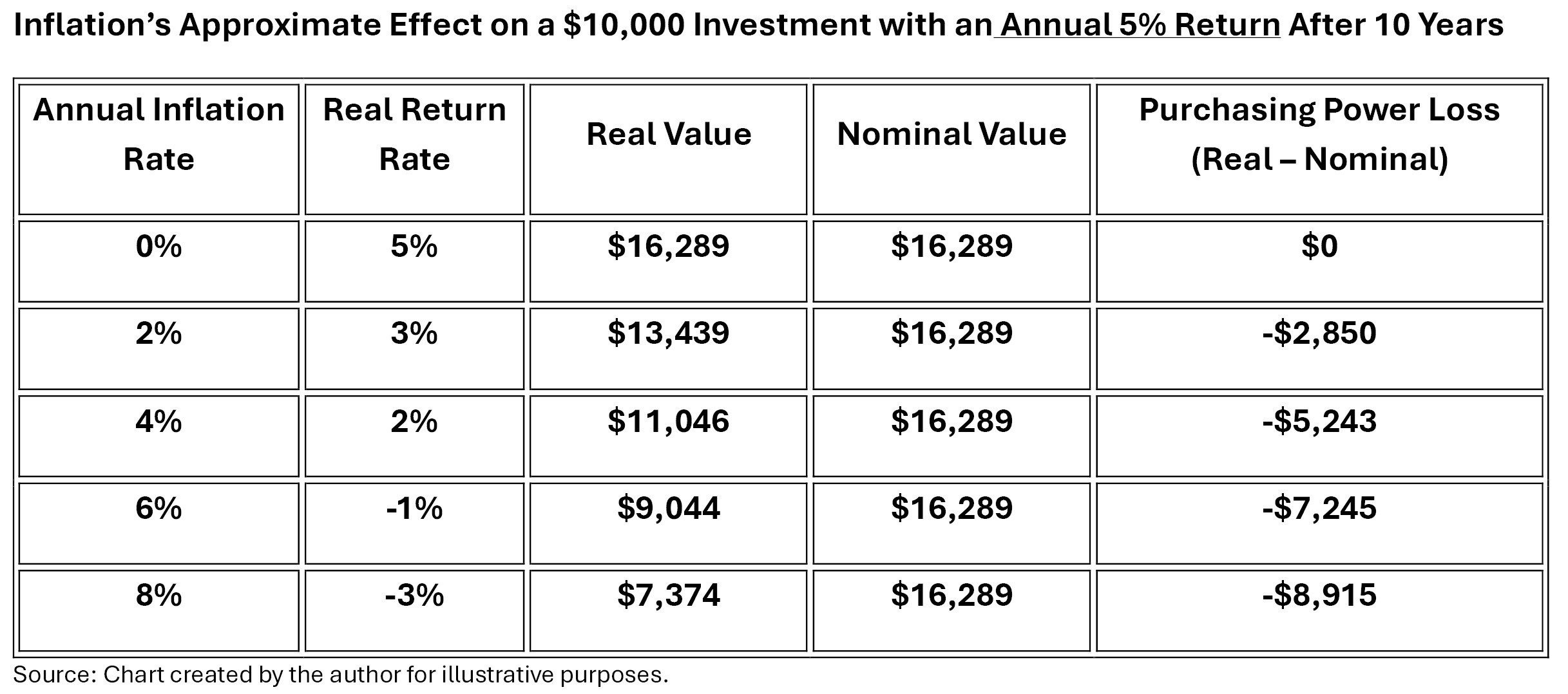

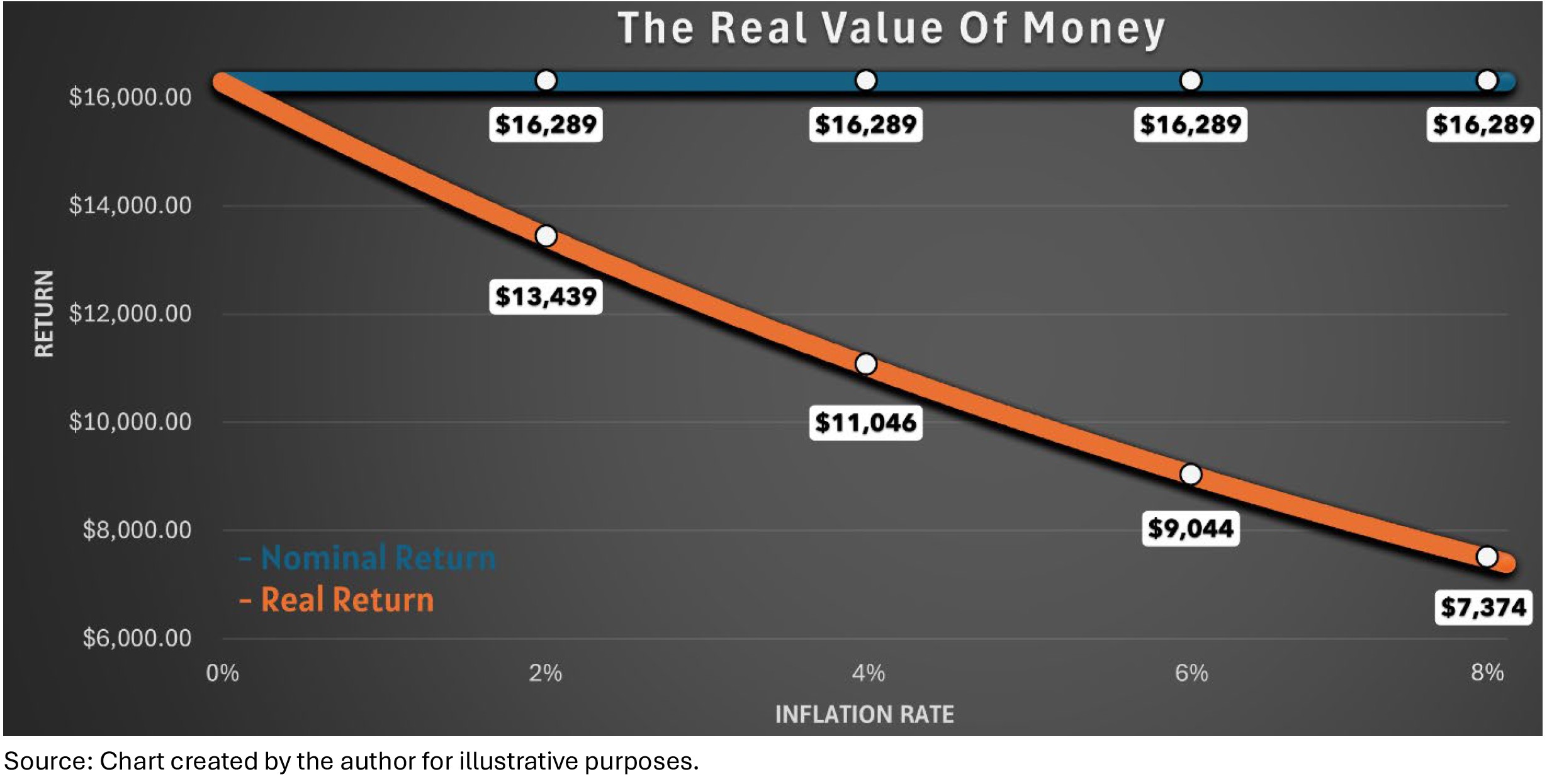

Inflation erodes your investment returns the same way it erodes your purchasing power. That’s why it’s important to understand the difference between one’s nominal return and real return. A nominal return is the amount generated by an investment excluding the effect of inflation, while a real return expresses one’s return including inflation’s effects. Over time, an investment’s after-inflation ("real") results depend on whether its returns keep pace with inflation. If your portfolio grows by 6%, but inflation is 4%, your real return is about 2% (Approximation: Real Return = Nominal Return – Inflation Rate). The table and accompanying graph below further demonstrate the importance of understanding inflation and its impact on your portfolio. One should note that these effects compound, leading to substantial discrepancies between the two values over time.

How do we measure inflation?

To measure inflation, statisticians utilize a price index. A price index entails creating and tracking the cost of a “market basket” of goods and services overtime. The goods and services are grouped into categories and assigned weights based on how a typical household spends its money, then statistical agencies compare the total cost of the basket from one period to the next.

In the United States, two primary price indexes exist:

- Consumer Price Index (CPI): Published by the Bureau of Labor Statistics. It focuses on out-of-pocket spending by urban households and is primarily used by government agencies for cost-of-living adjustments (COLAs) for items such as Social Security.

- Personal Consumption Expenditures (PCE): Issued by the Bureau of Economic Data Analysis. It covers a broader range of spending, including items paid on behalf of all households like employer-paid healthcare or Medicare, and it updates its market basket more frequently. The Federal Reserve generally emphasizes PCE as its inflation gauge for policy decisions.

Inflation and Retirement

Retirement is where inflation’s “invisible tax” tax can do the most damage regardless of age, as inflation has distinct effects for each demographic. Inflation pressures younger

individuals’ ability to save, while older individuals feel more pressure as their savings are more susceptible to the immediate impacts of purchasing power erosion.

Inflation pressures retirement through three common channels:

- The Income Effect: If everyday expenses rise faster than income, households may have to save less in order to maintain their standard of living.

- The Substitution Effect: As inflation rises, saving becomes less rewarding, so households typically substitute consumption instead of saving, similar to the income effect.

- The Wealth Effect: Higher inflation erodes the real value of assets, meaning one’s assets will be stretched thinner than anticipated.

These elements ultimately lead to a combination of eroded purchasing power and a lower propensity to save. The first two points were especially evident from 2021 to 2023 across all demographics, as a Boston College study found that 39% of surveyed individuals reported saving less due to inflation with about 25% suggesting they had to spend more from their savings due to their loss of purchasing power. On the other hand, one group was specifically impacted by the third effect: Retirees and near retirees.

This group is uniquely susceptible to inflationary pressure for several key reasons:

- More fixed income exposure: As investors approach retirement, portfolios often tilt toward bonds. Payments from nominal bonds do not adjust with inflation, and their prices typically fall when interest rates rise. While the stock market generally adjusts with inflation since their cash flows reflect increases in the products they sell, nominal bonds pay fixed payments and fall in value during inflationary periods.

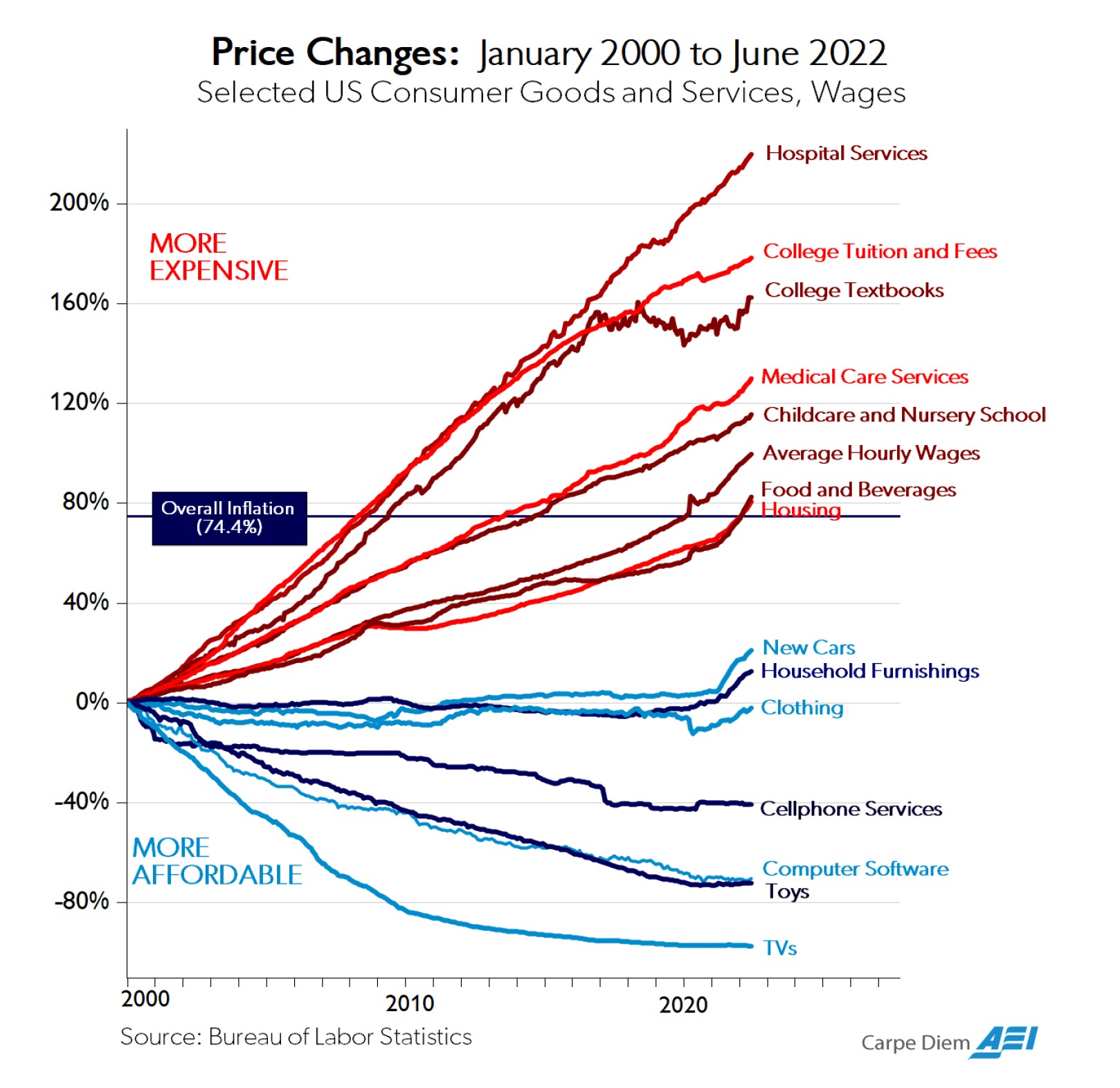

- More healthcare spending: Inflation doesn’t impact all goods and services the same. Medical costs have a history of rising faster than the overall inflation rate as seen below, and healthcare tends to take a bigger share of spending as we age.

- Less time to course-correct: Someone nearing or already in retirement has fewer years to rebuild purchasing power, so elevated inflation can substantially deteriorate a retiree’s nest egg if they are not adequately prepared.

Protecting Your Savings

Inflation is not something you can control, but you can build a plan that is more resilient to it. Below are several practical steps investors often consider:

- Stress Test Your Retirement Plan: Model multiple inflation scenarios and see what happens to your long-term purchasing power and withdrawal rate.

- Keep Growth in the Portfolio: Over long periods, stocks have historically provided one-way investors have sought to outpace inflation, though results vary and stocks involve risk, including loss of principal.

- Revisit your Withdrawal Rate during High Inflation: If costs jump, you may need to temporarily slow discretionary spending or adjust withdrawals to avoid depleting savings too quickly.

- Plan Explicitly for Healthcare: If you’re eligible, tools like Health Savings Accounts (HSAs) may offer tax advantages when used for qualified medical expenses. Consider consulting a qualified tax professional regarding your specific situation.

- Review Income Sources: Understand which income streams adjust for inflation (like Social Security COLA) and which do not (many private pensions).

We can’t control inflation, but we can plan for it. Consider discussing your personal situation with a qualified financial professional.

Disclosure:

This material is provided for informational and educational purposes only and should not be construed as investment, legal, or tax advice. The information presented is general in nature and may not be applicable to all investors or situations. Nothing herein should be interpreted as a recommendation to buy, sell, or hold any security or to adopt any particular investment strategy.

Any examples, illustrations, charts, or hypothetical scenarios are for illustrative purposes only and do not represent the performance of any actual client account or investment strategy. Hypothetical results have inherent limitations and do not reflect the impact of fees, taxes, transaction costs, or market conditions. Actual results may differ materially.

Investing involves risk, including the potential loss of principal. Past performance is not indicative of future results, and no guarantee can be given that any investment objective will be achieved.

Views and opinions expressed are as of the date of publication and are subject to change without notice. Readers should consult a qualified financial, legal, or tax professional regarding their individual circumstances before making any financial decisions.